Housing affordability has surged to the forefront of national discussions, reflecting a deep concern many Americans share about their ability to own a home. I've seen article after article like this one from CNN about young Americans giving up on ever owning a home. It's true, buying a home is difficult and has only been made more difficult in the past few years. Since 2020, the U.S. housing market has witnessed a significant transformation, primarily driven by various economic factors that have shifted the landscape of home ownership.

Notably, since the onset of the pandemic in early 2020, home prices have escalated dramatically. According to the National Association of Realtors, the median home price has increased by approximately 30% from 2020 to the end of 2023.

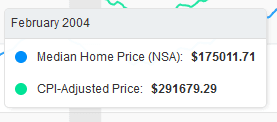

The median home price in 2004 was about $175,000. That number would be about $290,000 today adjusted for inflation. The current average home price in in the US today is around $397,000. Average income growth in that same period has gone from around $44,000 (around $70,000 adjust for inflation) to $74,000 in 2024. So, with a difference in home price of around $100,000 with hardly a meaningful difference in change in income (not to mention much higher inflation and other factors like massive student debt) it's easy to see why many aspiring homeowners are discouraged.

And as prices continue to rise, many have given up entirely. They fear they will continue to rent forever.

So, here is the central question. If you do not currently own a home, will you ever be able to afford one?

The answer is an absolute 100% YES, and here is how you will do it. We may not be getting as a good a deal as previous generations, but that doesn't mean there aren't proven strategies you can use to increase your buying power and by following this guide, I promise your ability to purchase a home will improve.

Section 1: Buy at the right time

Please, stick with me. I KNOW the biggest financial mistake you ever made was not buying a home in 1997 when you were 8 years old. But there is a point here, I promise you.

Many people have been hoping and praying for a market crash. Just because prices have increased, thy infer that a crash MUST be coming, because prices can't possibly stay this high.

After 2008, the threat of a crash is always POSSIBLE, but unlike back then we don't have an overabundance of people who cannot afford their home loans. We haven't seen a rise of foreclosures. A crash seems far-fetched in the near future.

In absence of a crash, how can we look for homes to become more affordable? How do we buy at the right time?

Home prices are primarily influenced by the fundamental economic principle of supply and demand. When there are more people looking to buy homes than there are homes available on the market, prices tend to rise. Conversely, if there are many homes available but fewer buyers, prices may drop.

The market can slow due to a number of factors including a rise in interest rates, an anticipated interest rate drop, the seasonality of the market or even a stretch of really bad weather.

This is important to note because as a potential buyer, you can use this to your advantage. When the market is slow, you have less options but much less competition. The demand is usually lagging, meaning as the market shifts supply doesn't quite meet demand immediately and you can use these market inefficiencies to score a really good deal. Maybe not pre-2020 pricing, but definitely something MORE affordable with near immediate equity when the market gets busier and prices begin to creep back up.

As a side note, the current market has seen a reduction in home values from the peak of 2022 due to "once in a lifetime" and "will never happen again" housing demand and interest rates. However, most people live in their home an average of 5 years. As the market returns to normal, even the people that bought at the top of the market are likely to see a return on their investment.

It's possible that prices continue to drop, HOWEVER, the sooner you purchase a home is generally better for pricing and long term equity building. And when we know it's a good time to buy NOW, it might get better and it might get worse. Either way, over the next 5+ years, you are likely to see your home value increase, which means more equity and more money in your pocket regardless of if your home value was down 12 months right after you purchased it.

Now, this alone might not be enough to make a difference, but if we continue to stack these best practices on top of each other, the cumulative effect can have a HUGE difference.

Section 2: Financial Strategies and Tools for Home Buyers

Once we have WHEN you should buy optimized, then let's look at HOW.

Let me start by saying if you are interested in purchasing a home AT ALL, you should meet with a trusted Mortgage Broker. I have several I work with that I can refer. They are free to meet with and give you a very detailed report of what you can afford based on your financial profile as it is currently and tell you the price of a home you can afford as well as your projected monthly payment. Many people I work with are often surprised at how much they can afford once they get pre-qualified for their loan, they could afford more than they thought!

That being said, not all of us have the cleanest financial profile and there are often ways we can improve our loan amount.

Factors that go into Loan Pre-Qualification

-

Income: Stability and amount of current income are crucial to show that you have the means to meet monthly mortgage payments.

-

Credit Score: A higher credit score can improve your chances of obtaining a loan with better interest rates and terms.

-

Debt-to-Income Ratio (DTI): This measures your total monthly debt payments against your gross monthly income. Lenders typically prefer a DTI ratio of 43% or lower.

-

Employment History: Lenders often look for a steady, reliable employment history to ensure that income is stable. Frequent job changes or gaps in employment can be red flags.

-

Assets and Savings: Besides your income, lenders will consider your savings, investments, and other assets. These can demonstrate financial health beyond regular income and can also affect down payment amounts and reserve requirements.

-

Down Payment: The size of the down payment can influence the terms of the loan, including the interest rate and whether you will need to pay for private mortgage insurance (PMI).

-

Property Type and Use: The type of property you are buying and whether it is your primary residence, a second home, or an investment property, can also affect loan eligibility.

Adjusting any of these factors can help increase your buying power. Increasing income may be tough, but you can always get a second person on the loan. If credit is a problem, there are many ways to improve your score. If saving for a down payment is difficult, there are ways to make a smaller payment as well. We will talk about that specifically in the next section. And if one of these areas is not great and proving difficult to improve, that doesn't stop you from obtaining financing and improving the OTHER areas will have a great impact.

And again, it's FREE to find out your purchasing power!

Section 3: The Government Can Help

...Stick with me here. I'm giving you every tool in the bag

If you are still having trouble qualifying for a loan, various government programs and assistance can provide valuable support. These initiatives are designed to make homeownership more accessible and affordable through loans, grants, and tax incentives.

Federal and State Assistance Programs for First-Time Home Buyers

Both federal and state governments offer numerous programs to assist first-time home buyers. For instance, the U.S. Department of Housing and Urban Development (HUD) provides resources and assistance programs that vary by state, including grants for down payment assistance and subsidized loans for low-income buyers. Many states also offer similar assistance programs, which can include additional benefits such as lower interest rates for first-time buyers, assistance with closing costs, or educational programs aimed at helping new buyers understand the home purchasing process.

Benefits of FHA Loans, VA Loans, and Other Government-Backed Mortgages

Government-backed loans are designed to lower the barriers to homeownership for many Americans:

-

FHA Loans: The Federal Housing Administration (FHA) offers loans that require lower minimum credit scores and down payments as low as 3.5% of the home’s purchase price. FHA loans are a popular choice for first-time buyers and those with less-than-perfect credit.

-

VA Loans: Available to veterans, active-duty service members, and some members of the National Guard and Reserves, VA loans are provided by private lenders but guaranteed by the Department of Veterans Affairs. These loans offer competitive interest rates and do not require a down payment or private mortgage insurance (PMI), which can significantly reduce monthly payments.

-

USDA Loans: Targeted at buyers in rural and some suburban areas, U.S. Department of Agriculture loans are another option that requires no down payment and offers lower interest rates.

These programs not only make it possible for more people to afford a home but also often come with more favorable payment terms, which can be a tremendous long-term benefit.

Tax Incentives for Home Buyers

The U.S. tax code offers several incentives that can make buying a home more affordable. One of the most significant is the ability to deduct mortgage interest from your federal income taxes. This deduction can lower your taxable income, potentially saving you a significant amount of money each year. Additionally, some states offer tax credits for first-time home buyers, which directly reduce the amount of tax owed, further lowering the cost of buying a home.

Homeowners may also qualify for other tax benefits, such as property tax deductions and federal tax credits for energy-efficient upgrades and renovations. These incentives not only help reduce the initial costs of buying a home but also encourage ongoing investment in housing.

In Texas, we also have something called a Homestead Exemption, where your property taxes are not allowed to increase more that 10% in any given year on your primary residence. This may not sound great at first, but the longer you own a home, the more it will increase in value and the more taxes you will owe. UNLESS you file your homestead exemption! Another reason to purchase as soon as your able.

Section 4: Let's Get Creative - Alternative Home Buying Options

For many prospective homebuyers, traditional paths to purchasing a home—such as saving for a large down payment and securing a conventional mortgage—may not always be feasible. Exploring less traditional routes can open up new possibilities and opportunities to enter the housing market. Here’s a look at some alternative strategies that can help make home ownership more attainable.

Exploring Less Traditional Routes: Co-ownership, Rent-to-Own Schemes, and Buying at Auction

-

Co-ownership: This option involves partnering with friends, family members, or investors to purchase a property together. Co-ownership allows individuals to share the financial burden of buying and maintaining a home, making it more affordable for each party. Legal agreements are crucial in this arrangement to outline each person's responsibilities and what happens if someone wants to sell their share, but it's a way to build equity.

-

Rent-to-Own Schemes: These programs allow renters to build equity in a home through lease payments, with a portion of each payment going toward a future down payment to eventually buy the house. Rent-to-own can be a viable option for those who are not yet ready to secure a mortgage due to credit issues or lack of down payment. Usually will have to be negotiated with a home seller rather than a traditional lender.

-

Off Market Homes: Purchasing a home "off market" means one not listed on the Multiple Listing Service and not syndicated out to websites like Zillow and Realtor.com. This is an option to get a below-market deal in desirable areas. Harder to do, but can be a gamechanger.

In addition to these strategies, you can always just look for a less desirable home. It wont be the best option for many, but can end up being VERY lucrative.

Benefits of Considering Fixer-Uppers or Properties in Emerging Neighborhoods

-

Fixer-Uppers: Although they require more initial work, fixer-uppers can be bought at a lower price point, offering a potentially significant return on investment after renovations. For those who are handy or have access to affordable contracting services, fixer-uppers provide a way to gradually build equity while personalizing a home to your preferences.

-

Emerging Neighborhoods: Buying in an up-and-coming area can also be a strategic move. Properties in these regions are typically more affordable and have a higher potential for appreciation in value as the neighborhood develops.

Exploring these alternative home buying options can offer viable paths to homeownership for those who find the traditional process challenging, providing creative solutions to build equity and achieve residential stability.

Section 5: Real Estate VS Other Investments

There has been a rise recently in regarding real estate as a bad investment when compared to other financial instruments. While it may not offer the crazy high potential returns of crypto currency or day trading shenanigans, real estate has traditionally been seen as a sound long-term investment, providing both appreciable value and functional utility. This dual benefit—where one can live in or use the asset while it appreciates—sets real estate apart from other investment types. Understanding historical trends and the comparative advantages of real estate investment allows buyers to make informed financial decisions aligned with their long-term goals.

Historical Data on Real Estate as a Long-Term Investment

Historically, real estate has proven to be a reliable investment, with property values generally increasing over time. According to the Federal Housing Finance Agency, house prices have risen by an average of 3.4% annually from 1991 to 2020. I chose to look at pre-pandemic specifically to avoid the crazy outlier appreciation many have experienced. This consistent appreciation not only helps in wealth accumulation but also serves as a hedge against inflation, ensuring that the real value of the property does not diminish even when currency values fluctuate.

Over extended periods, despite the cyclical nature of real estate markets, property values have tended to recover from declines and reach new highs, making real estate a resilient investment. Despite the recent wackiness, as the market becomes more normal (which may be soon) we can expect to see this type of growth again.

The Potential for Home Equity Growth Over Time

Home equity—the difference between the property's value and the mortgage balance—increases as homeowners make regular mortgage payments and as the property value appreciates. This growth in equity can be significant, especially in appreciating markets. Homeowners can leverage this equity for financial advantages such as refinancing at better rates, securing home equity loans, or further property investments. The tangibility and usability of real estate also mean that while you are investing, you are also residing in or utilizing the asset, whether as a primary residence or a rental property. Equity is the main driver to getting the wealth ball rolling.

Real Estate vs. Other Types of Investments

Compared to stocks, bonds, or other securities, real estate offers several distinct advantages:

-

Tangibility and Control: Unlike stocks, real estate is a tangible asset that investors can physically enhance or improve, directly influencing its value and potential rental income.

-

Usability: One of the unique aspects of real estate is its usability. As a homeowner, you benefit not just from the asset's appreciation but also from its utility as a living space. This dual function—where your investment also provides daily benefits—adds a layer of value that other investment vehicles do not offer.

-

Rental Income: Real estate can generate ongoing rental income, which can cover the expenses associated with the property and provide additional income. This income stream, coupled with long-term capital appreciation, underscores the dual financial benefits of real estate.

-

Tax Advantages: Real estate investing offers tax deductions that can significantly reduce the cost of ownership and improve net returns. These include deductions for mortgage interest, property taxes, operating expenses, depreciation, and favorable capital gains treatment.

-

Inflation Hedge: Real estate naturally acts as a hedge against inflation. As inflation increases, so typically does the value of property and the amount landlords can charge for rent, thereby maintaining the purchasing power of the investment over time.

By embracing a long-term perspective, investors in real estate not only secure a usable asset that appreciates but also benefit from its potential for generating income, its tax advantages, and its role in a diversified investment strategy. These factors make real estate a robust component of any investment portfolio, particularly for those seeking stable, long-term financial growth.

Section 7: The Math

Ok, let's put it all together. The math might get a little complicated (AI helped me out here a lot) but that makes these numbers very accurate.

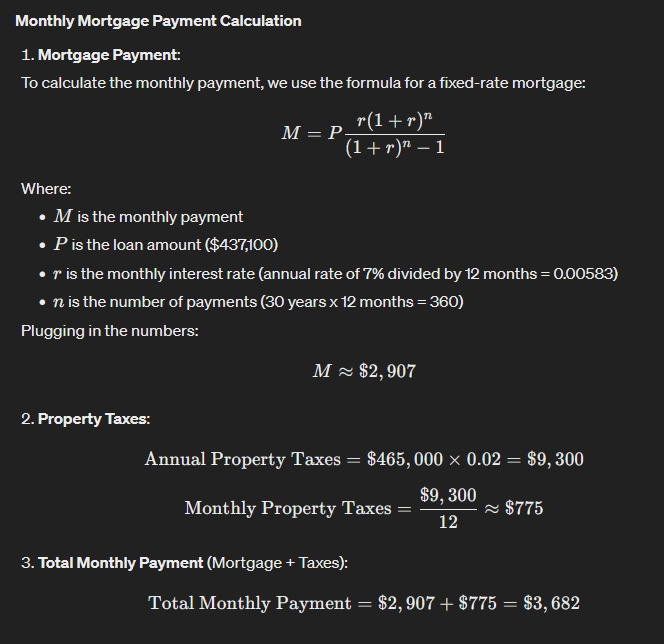

To better understand what it takes for the average American to buy a home in Austin with a median price of $465,000, let's break down the numbers, including income requirements, debt, interest rates, down payment, monthly mortgage payments, and potential home equity growth over five years.

Scenario Setup

-

Median Home Price in Austin: $465,000

-

Interest Rate: 7% (assumed based on current trends)

-

Credit Score: Good to great (assumes qualification for the stated interest rate)

-

Average Savings/Down Payment: These days, first-time homebuyers put down about 6% of the home price. For a $465,000 home, that's $27,900.

-

Loan Amount: $437,100 (after down payment)

-

Loan Term: 30 years

- Property Taxes: Approximately 2% annually of the property's assessed value (depending on where you live)

Monthly Mortgage Payment Calculation

This would make your average monthly mortgage payment around $3,682.

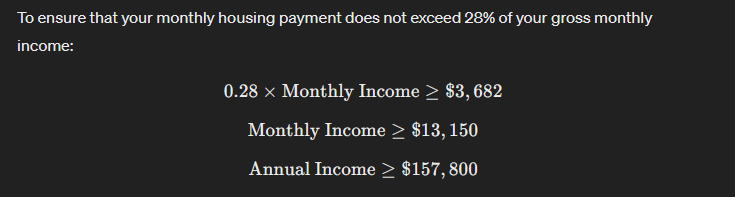

Income Requirement

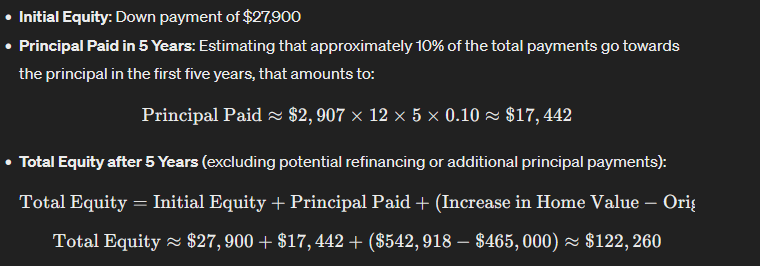

Forecast Home Value in 5 Years

Estimated Equity Buildup

So, the one problem with this scenario is it does call for an income of around $158,000. For reference, the median household income in 2022 was $110,300. For some in Austin, that is no problem whatsoever. But for others, I recognize that this is a high income. This is where our other factors come in. If your married, maybe your income plus your spouse makes up this gap. Maybe we use those tips we talked about to earlier to get something LESS than the median value in Austin to build equity over the next few years. If you don't want to be so highly leveraged, maybe consider one of the surrounding areas like Kyle or Leander that more affordable but still very nice homes.

Whichever path you take, you will ALWAYS be able to take the equity from the home you own and leverage it into a more expensive home down the road.

The goal of this demonstration was to show that the average home in Austin will net you around $122,000 in equity for living in it. Keep in mind, when you go to sell and purchase your next home, this is money you can use for an even larger down payment, something you can borrow against for a HELOC, or move down to a less expensive home and pocket your profit. The possibilities are endless.

I think that is the best case possible for buying a home, and it is all made possible by the average homebuyer.

Section 8: The Value of Partnering with a Real Estate Agent

As you can see, buying a home is an attainable goal for most people, but it is still complicated. This is just the financing and affordability side of the equation!

It may seem self serving, but when navigating the complexities of the real estate market, partnering with a knowledgeable real estate agent can be invaluable.

Expert Guidance and Market Knowledge

Real estate agents bring a wealth of knowledge and expertise about property markets, which is crucial for making informed decisions. They understand historical market trends, current conditions, and future projections, allowing them to provide strategic advice on when and where to buy. An experienced agent can interpret data on market prices, inventory levels, and community developments, guiding buyers through complex market dynamics to find the best opportunities.

Access to Off-Market Deals

One of the significant advantages of working with a professional is our access to off-market listings, sometimes known as "pocket listings." These properties aren't available on public listings and can often present more affordable options for buyers. Agents leverage their extensive networks to connect their clients with these exclusive opportunities, often in competitive markets where getting ahead of the public listings can make the difference in securing a home.

Negotiation Skills

Real estate agents are skilled negotiators, trained to secure the best possible price and terms on behalf of their clients. With an agent's negotiation expertise, buyers can save thousands of dollars—a critical advantage in high-stakes property negotiations. Agents understand the legalities and can handle objections or counteroffers effectively, ensuring that the financial interests of buyers are protected.

Streamlining the Buying Process

The process of buying a home involves numerous steps, including legal paperwork, financing, inspections, and closing procedures. Real estate agents streamline these complexities by handling much of the administrative and coordination work. This support is especially beneficial for first-time buyers unfamiliar with the process. Agents ensure that all necessary documents are completed correctly, deadlines are met, and the transaction progresses smoothly toward closing.

Local Insights and Network

Agents provide invaluable local insights into neighborhoods, schools, and amenities, helping buyers make educated decisions about where they choose to live. They often have detailed knowledge about planned developments, local zoning laws, and community dynamics. Additionally, an agent's network can be a treasure trove of information and resources, including insights into properties about to hit the market and recommendations for service providers.

Professional Network

A real estate agent's professional network includes relationships with mortgage brokers, home inspectors, appraisers, and legal professionals who can facilitate the various aspects of the buying process. These connections can expedite the transaction, ensure thorough due diligence, and provide buyers with competitive service options. This network is particularly valuable in streamlining financing and closing processes, which can be daunting for those unfamiliar with real estate transactions.

This is all to say, a professional and experienced agent will save you money (and help prevent you from losing it) which only furthers your purchasing power.

Given the recent NAR settlement, buyers agents may actually become more expensive for the client to use (we will touch more on that in a later post). But I firmly believe that if you are concerned about your ability at all to purchase a home, a good real estate agent is invaluable to you.

Conclusion: Yes, You Can Own a Home

Despite the daunting headlines and soaring prices, owning a home in today's market is not only possible—it's entirely achievable. While challenges exist, they are not insurmountable. The key lies in understanding the market, leveraging the right financial strategies, and utilizing all available resources. Remember, the journey to homeownership is a marathon, not a sprint, and with the right approach and guidance, you can cross the finish line.

The reality is that every generation faces its unique set of economic conditions and market dynamics; today's buyers are no different. Yet, history has shown that with perseverance and smart planning, buying a home remains one of the most steadfast investments one can make. It's not just about having a place to live; it's about securing your financial future and building a legacy.

So, if you feel overwhelmed by the process or unsure where to start, you're not alone. This is where partnering with a knowledgeable real estate agent can make all the difference. An experienced agent can provide you with the market insights, negotiation skills, and personalized guidance necessary to navigate this complex landscape successfully.

Don't let fear or uncertainty hold you back. Owning a home is within your reach, and the right help is just around the corner. If you're ready to take the first step or simply want to explore your options, I invite you to book a free buyer's consultation with me. Together, we can chart a path to your new home with confidence and clarity.

Book your free consultation today and let’s turn your home ownership dreams into reality.